Asian equities staged a broad relief rally on Wednesday as Brent crude slipped below the $100-per-barrel threshold, easing immediate concerns over war-driven supply disruptions and offering investors a temporary reprieve from inflation fears tied to the Iran conflict. The move followed renewed expectations that U.S. military operations linked to the fifth week of the war could wind down within two to three weeks, a development that materially reduced the geopolitical risk premium embedded in energy markets.

The dominant market angle was cross-asset reaction to geopolitical de-escalation, with lower oil prices directly feeding gains in export-heavy Asian bourses and improving risk sentiment after Wall Street’s strongest session in nearly a year.

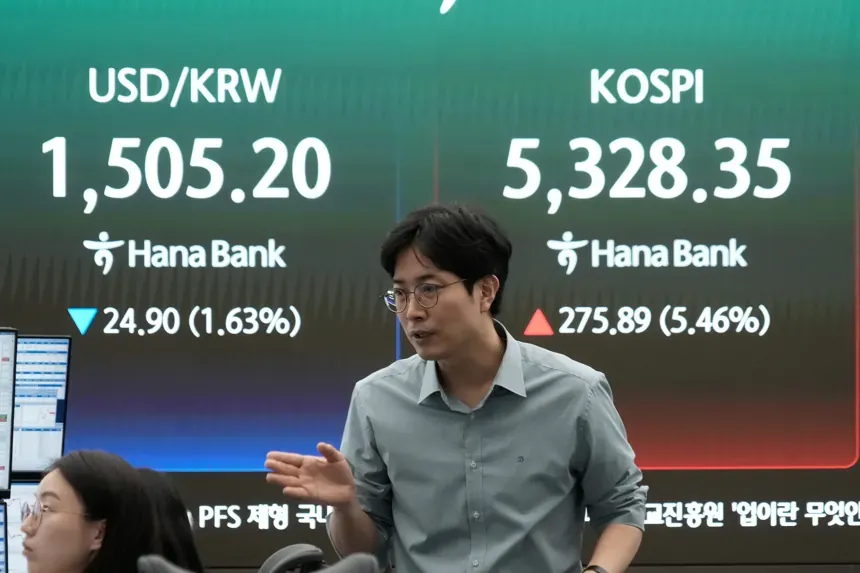

Energy retreat drives regional equity rebound

Brent crude declined 4.4% to $99.44 a barrel, while U.S. benchmark West Texas Intermediate fell 3.8% to $97.55, according to market pricing cited by AP. The drop reversed part of the sharp risk premium built into crude during weeks of disruption near the Strait of Hormuz, the maritime chokepoint that handles roughly one-fifth of global oil flows.

Asian stock markets responded decisively. South Korea’s Kospi surged 8.4%, Tokyo’s Nikkei 225 advanced 5.2%, and Taiwan’s Taiex gained 4.6%, as investors rotated back into cyclical and technology-linked names that had been pressured by elevated energy costs and fears of margin compression.

Hong Kong’s Hang Seng rose 2.3%, mainland China’s Shanghai Composite added 1.5%, while India’s Sensex climbed 2.4%, underscoring the breadth of the rebound across the Asia-Pacific region.

The market response suggests investors are recalibrating expectations for near-term inflation trajectories, particularly in import-dependent Asian economies where fuel costs feed quickly into logistics, manufacturing, and consumer pricing.

Macro implications extend beyond oil

The decline in crude prices may offer modest relief for central banks monitoring war-related inflation spillovers. Earlier this week, U.S. gasoline prices had moved above $4 per gallon for the first time since 2022, reinforcing concerns that the conflict could delay monetary easing cycles globally.

A parallel boost came from domestic data in Japan, where a Bank of Japan survey showed improved sentiment among major manufacturers despite weeks of geopolitical uncertainty. That data point added a macroeconomic foundation to the equity rally beyond purely sentiment-driven gains.

Still, economists cautioned that even a formal military de-escalation may not fully unwind the supply-chain and freight disruptions already set in motion across shipping routes linked to the Gulf.

Wall Street strength reinforces global risk appetite

The rebound in Asia followed a strong lead from U.S. markets, where the S&P 500 rose 2.9%, the Dow Jones Industrial Average gained 2.5%, and the Nasdaq Composite climbed 3.8% in Tuesday trading. The gains reflected renewed appetite for growth sectors once the probability of prolonged oil shocks began to ease.

Semiconductor and healthcare deal activity also supported the broader tone. Nvidia gained after disclosing a $2 billion investment in Marvell Technology, while Eli Lilly announced an acquisition of Centessa Pharmaceuticals, reinforcing a risk-on backdrop for equities.

The combination of falling crude, stronger U.S. equities, and improved Asian manufacturing sentiment points to a market increasingly pricing a shorter-duration geopolitical shock, though volatility around Hormuz shipping security remains a critical variable for the next trading sessions.